How to Transform Your Finances: A Simple 30-Day Financial Reset Plan That Actually Works

Are you ever surprised at how quickly your paycheck disappears each month? You’re not alone. Managing money can feel overwhelming, but it doesn’t have to stay that way. A focused 30-day financial reset can help you take control, build better habits, and create long-lasting financial stability—one simple step at a time.

What Is a Financial Reset?

A financial reset isn’t about extreme budgeting or depriving yourself. It’s about creating intentional habits that compound over time. By dedicating just 30 minutes a day to your finances, you can identify spending leaks, automate routine tasks, and build systems that work even while you sleep.

Imagine saving an extra $120–$260 every month just by making small, intentional changes. That’s the power of a 30-day reset—it gives you momentum and clarity without requiring drastic life changes.

Start Today, Not Tomorrow

Forget waiting for Monday or January 1st. Research shows that the “perfect time” myth only delays progress. Unlike quick fixes that fade fast, financial transformation comes from consistent daily actions that grow stronger over time.

Even a focused 30-minute session can create meaningful change. By organizing your finances, negotiating bills, and trimming unnecessary spending, you’ll see results quickly—and they will compound.

The Purpose and Mindset of a Financial Reset

A reset provides a fresh start, reducing mental fatigue caused by constant money decisions. Think of it as hitting the pause button on financial stress to gain clarity and direction.

Many avoid reviewing finances because it feels overwhelming. A structured reset breaks this cycle with manageable steps, making it perfect for times of life change—marriage, career shifts, or mounting debt.

Tip: Keep a money journal during your reset. Note practical observations like, “I spend $80 per week on takeout,” and emotional responses like, “I feel anxious checking my bank account.” This practice helps you understand both habits and emotional triggers.

Week 1: Track and Review – Understand Where Your Money Goes

The foundation of a successful financial reset is understanding your current situation. Gather bank statements, credit cards, investment accounts, and debt info, then compare your income with expenses.

Start a daily spending log to capture every purchase. You might uncover $75 in forgotten subscriptions or $200 in impulse spending. This is data collection, not self-criticism—approach it with curiosity. Without this step, planning your financial journey is like navigating without a map.

Week 2: Organize and Automate – Streamline Your Financial Life

Once you know where your money goes, it’s time to create systems that reduce stress.

- Organize bills and set up automatic payments to avoid late fees.

- Establish a simple budget to create spending boundaries.

- Use digital tools to track expenses effortlessly.

Automation is your secret weapon. By removing daily decision-making on bills and savings, you free up mental energy for bigger financial strategies.

Week 3: Optimize and Trim – Cut Unnecessary Spending

Week three focuses on finding money you didn’t realize you had:

- Cancel unused subscriptions—most people save $20–$50 monthly.

- Negotiate essential bills—a quick call can save $10–$40.

- Reduce food costs by planning meals and limiting takeout, saving $60–$100.

- Review banking and insurance fees for extra savings.

Ask yourself: “Does this expense align with my values?” Prioritize spending that truly matters.

Week 4: Plan and Save – Set Goals for Your Future

The final week focuses on building for long-term stability:

- Emergency fund: aim for three months of essential expenses.

- Automate savings: weekly transfers of $50 plus 10% of extra income.

- Prepare for upcoming expenses like holidays or annual bills.

- Explore ways to increase income through side hustles or selling unused items.

This final step ensures that your reset sets the foundation for ongoing financial success.

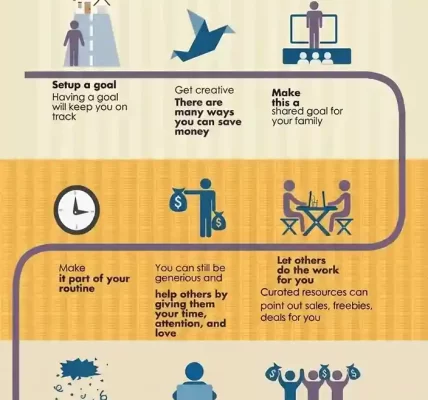

Staying Accountable and Motivated

Consistency is key. Try these strategies:

- “Money Thursday” check-ins: 3 minutes to review spending and celebrate wins.

- Track both numbers and emotions to understand your financial behavior.

- Set calendar reminders for bills and check-ins.

- Celebrate small victories like paying off $50 in debt or negotiating a $10 discount.

Overcoming Common Obstacles

- Decision fatigue: focus on one financial priority at a time.

- Feeling overwhelmed: break tasks into 10-minute segments.

- Life changes are normal—adapt your reset to stay sustainable.

Remember, your 30-day reset is flexible and forgiving. It’s designed to evolve with your life.

When to Seek Professional Help

Sometimes outside expertise is necessary. Consider professional guidance if:

- Debt consumes most of your income

- You manage multiple high-interest credit cards

- You’re unsure how to rebuild credit

- Retirement planning feels impossible

Financial counselors offer objective advice without judgment and can help create realistic, personalized strategies.

Small Steps Lead to Big Results

Your 30-day reset is just the beginning. Consistent, small changes—tracking expenses, automating savings, trimming unnecessary spending—build lasting results.

Even small daily savings add up: $5 a day becomes $1,825 annually, enough to boost your emergency fund or reduce debt. Think of this reset as training wheels for financial independence. Repeat it whenever needed to maintain momentum.

Your Financial Journey Starts Today

Financial wellness isn’t about perfection—it’s about progress. Each small action compounds over time, building confidence and control. Track expenses, cancel unused subscriptions, automate savings—and watch your financial habits transform.

Why wait for tomorrow when your path to financial clarity can start today?

Disclaimer: This blog is for educational purposes only and is not financial, legal, tax, or investment advice. Individual circumstances vary; consult a qualified professional before making financial decisions.