Building an Emergency Fund From Zero: A 12-Month Blueprint

Creating an emergency fund is one of the smartest financial steps you can take. It provides a safety net for unexpected expenses like medical bills, car repairs, or temporary income loss. But how do you go from zero to a fully funded emergency fund in just 12 months? This comprehensive guide offers a step-by-step plan, practical tips, and expert advice to make it achievable.

Why a 12-Month Timeline Works

A 12-month plan is long enough to make significant progress, yet short enough to keep motivation high. By spreading your savings across a year, you can:

- Build a consistent habit of saving

- Test spending adjustments without feeling deprived

- Achieve a 3–6 month reserve of essential expenses

For freelancers or gig workers, aiming for 6–12 months is safer due to variable income.

Step 1: Calculate Your Emergency Fund Target

Start by totaling your essential monthly expenses, including:

- Housing (rent/mortgage)

- Utilities

- Groceries

- Insurance

- Minimum debt payments

- Transportation

- Childcare

Exclude discretionary spending like dining out, streaming subscriptions, and hobbies.

Example Calculation:

| Monthly Essentials | $2,500 |

| 3 months reserve | $7,500 |

| 6 months reserve | $15,000 |

Tip: Use an emergency fund calculator to personalize your target.

Step 2: Set a Realistic Monthly Savings Goal

Divide your total target by 12 to establish your monthly contribution. If this feels too ambitious, start with a smaller milestone:

- Primary goal: Save one month’s essentials in the first 3 months

- Secondary goal: Reach your full 3–6 month target in the remaining 9 months

Example Plans:

- Aggressive: $15,000 → $1,250/month

- Moderate: $7,500 → $625/month

- Starter: First milestone $1,000 → ~$335/month

Step 3: Find the Money (Months 1–3)

Focus on three income paths:

- Reduce Expenses: Cancel unused subscriptions, renegotiate bills, and cut small discretionary spending.

- Increase Income: Take on overtime, side gigs, or sell unused items.

- Reframe Windfalls: Allocate bonuses, tax refunds, or stimulus checks directly to your fund.

Small changes, like skipping two restaurant meals weekly, can free up hundreds of dollars monthly.

Step 4: Automate and Separate (Months 1–12)

Open a dedicated, FDIC-insured or NCUA-insured savings account. Set up automatic transfers aligned with your paydays.

Why it works:

- Reduces temptation to spend

- Simplifies tracking progress

- Automation accelerates growth—clients often hit goals 40–60% faster

Keep funds liquid but safe. High-yield savings accounts and money market accounts are ideal.

Step 5: Use a Tiered Savings Approach

Divide your fund into three tiers:

- Immediate Cash Buffer ($500–$1,000): Instant access for minor emergencies.

- Primary Emergency Fund (Rest of 3–6 months): High-yield savings or money market account.

- Recovery Bucket (Optional): For freelancers/self-employed, short-term CDs or municipal debt for less immediate access.

This balances accessibility, safety, and modest interest returns.

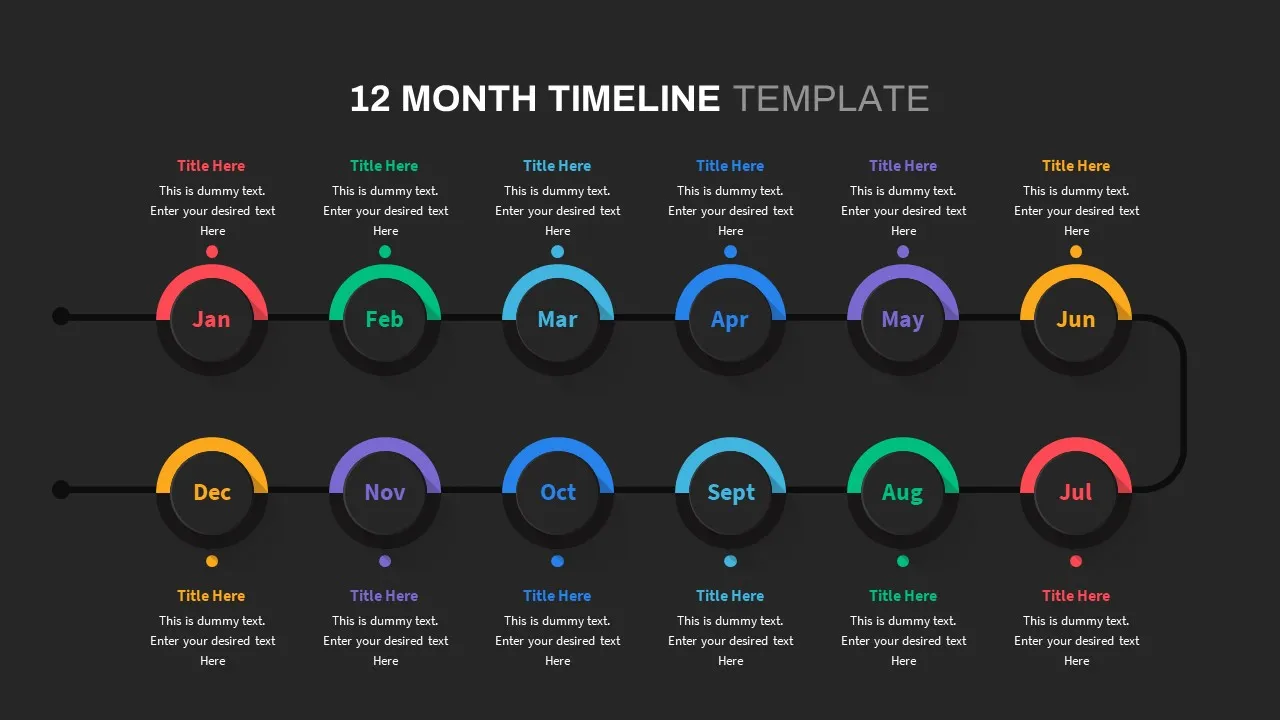

Sample 12-Month Blueprint

| Month | Action | Goal (example $7,500 target) |

| 1 | Calculate expenses, open account, automate transfer | $625 |

| 2 | Apply windfall or bonus | $1,250 |

| 3 | Trim subscriptions, add side gig income | $1,875 |

| 4 | Reassess bills for savings | $2,500 |

| 5 | Redirect bonus/tax refund | $3,125 |

| 6 | Mid-year review, increase transfer if possible | $3,750 |

| 7–11 | Continue automatic savings | $5,625 |

| 12 | Reach target and celebrate | $7,500 |

Adjust contributions based on your personalized target.

Where to Keep Your Emergency Fund

- High-yield online savings accounts

- Money market accounts

Avoid: stocks or long-term bonds (principal risk), or cash “under the mattress” (uninsured).

Interest earned is taxable as ordinary income—track deposits for tax reporting. Consult a benefits counselor if large balances affect eligibility for means-tested programs.

Common Mistakes to Avoid

- Using the fund for non-emergencies

- Chasing high returns with risky investments

- Keeping money in unbanked or uninsured locations

- Setting an unrealistic target

When to Use Credit Instead

For planned, small purchases (like a car repair with 0% financing), using low-cost credit may be better than depleting your fund. Avoid high-interest loans, and always compare costs before deciding.

Behavioral Tips That Work

- Keep your goal visible (apps, spreadsheets, or a jar)

- Automate savings before spending

- Reward milestones: 25%, 50%, 75%, 100%

Special Situations

- Freelancers or small-business owners: target 6–12 months, possibly separate business reserves

- Families with dependents: aim for larger reserves

- Job transitions: temporarily increase the buffer

Real-World Examples

- Young Couple: Cut $300/month, automated $700/month → $10,000 fund in 12 months

- Single Parent: Started $100/month, added tax refund and gigs → $4,800 in 1 year

Maintaining Your Fund After Year One

- Reassess annually for lifestyle or job changes

- Keep a one-month cushion automatically

- Use surplus for sinking funds or investments