Managing your money doesn’t have to be complicated. One of the most popular and beginner-friendly budgeting methods is the 50/30/20 rule—a simple framework that helps you divide your after-tax income into three essential categories: needs, wants, and savings.

In this guide, you’ll learn how the 50/30/20 rule works, see real examples, and discover its pros and cons so you can decide if it’s right for your financial journey.

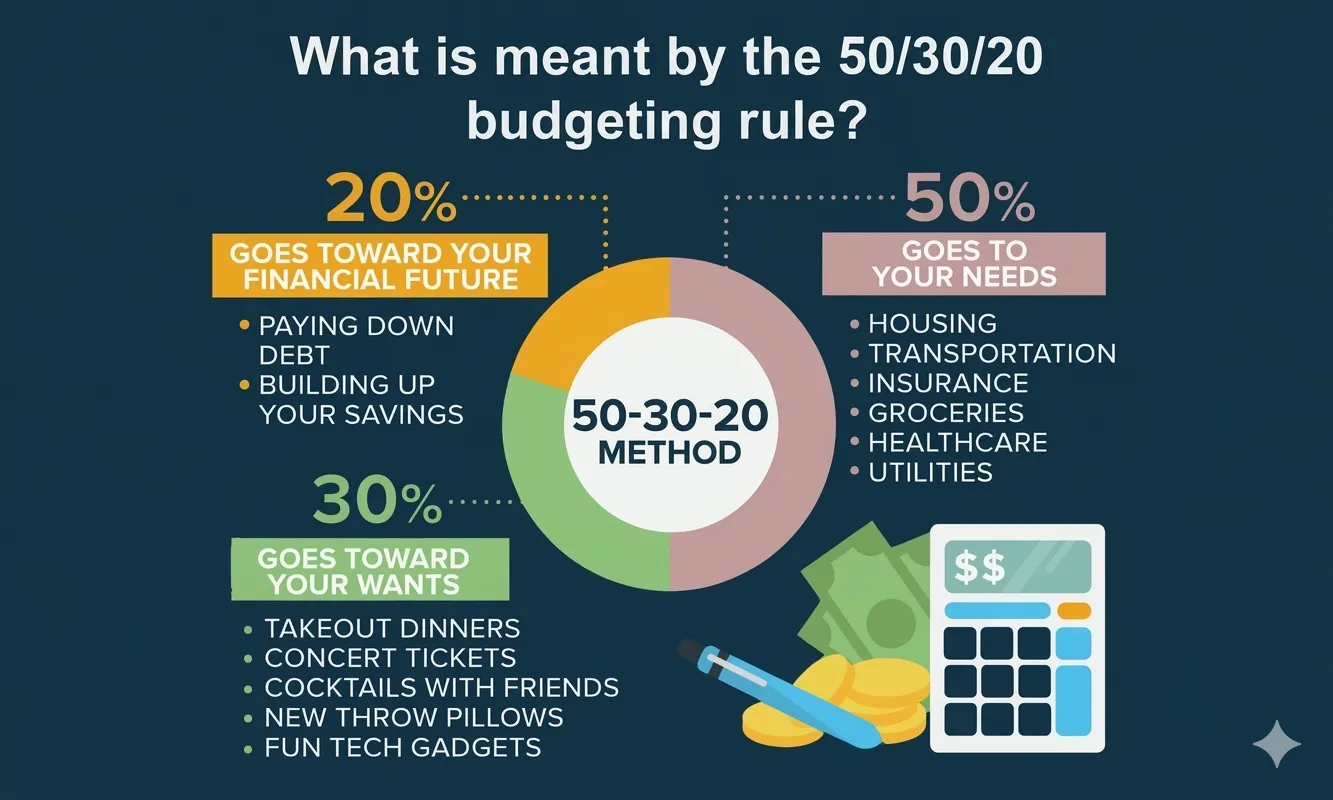

The 50/30/20 Rule Explained

What Is the 50/30/20 Rule?

The 50/30/20 rule is a budgeting strategy that allocates your income as follows:

- 50% for Needs

- 30% for Wants

- 20% for Savings and Debt Repayment

Instead of tracking every single expense, this method focuses on broad spending categories—making it ideal for beginners or anyone looking for a simple way to manage money.

1. Needs (50%) The 50/30/20 Rule Explained

“Needs” are essential expenses required for basic living. These are non-negotiable costs that keep your life running.

Common examples include:

- Groceries

- Rent or mortgage payments

- Utilities (electricity, water, internet)

- Transportation

- Healthcare

- Minimum debt payments

Depending on your situation, needs may also include childcare or financial support for family members.

Important tip:

Just because something is a “need” doesn’t mean you shouldn’t control the cost. For example, you need housing—but that doesn’t mean buying a home beyond your budget is a good idea.

2. Wants (30%) The 50/30/20 Rule Explained

“Wants” are expenses that improve your lifestyle but aren’t essential for survival.

Examples of wants:

- Dining out

- Vacations

- Gifts

- New clothes

- Streaming subscriptions

- Electronics (TVs, laptops, etc.)

Wants are not wasteful—they add joy and comfort to life. However, if your income drops, these are the first expenses you should reduce or eliminate.

3. Savings (20%)

The final 20% of your income goes toward building your financial future.

This includes:

- Emergency fund

- Investments or brokerage accounts

- Retirement savings

- Extra debt payments (beyond minimums)

- Student loans or car payments

This category is all about delayed gratification—sacrificing some spending today to create long-term financial security.

50/30/20 Rule Example

Let’s say your monthly after-tax income is $8,000. Using the 50/30/20 rule, your budget would look like this:

- $4,000 for needs (50%)

- $2,400 for wants (30%)

- $1,600 for savings (20%)

Over one year, saving $1,600 per month would give you $19,200—a strong financial cushion for emergencies or investments.

Benefits of the 50/30/20 Rule

Simple and easy to follow

You don’t need complex spreadsheets or detailed tracking systems.

Beginner-friendly

Perfect for those new to budgeting or overwhelmed by financial planning tools.

Encourages saving

It builds a habit of consistently setting aside money for the future.

Builds financial confidence

Success with a simple system can improve your belief in your ability to manage money—also known as financial self-efficacy.

Drawbacks of the 50/30/20 Rule

May not be realistic for everyone

In many cases, essential expenses exceed 50%—especially for families or those living in expensive areas.

Too rigid

Life is unpredictable. Fixed percentages don’t always adapt well to changing expenses like medical bills or seasonal costs.

Limited flexibility

Unlike zero-based budgeting, this method doesn’t allow detailed adjustments for specific financial goals or situations.

Who Should Use the 50/30/20 Rule?

This budgeting method works best if you:

- Are new to managing money

- Have relatively low essential expenses

- Prefer a simple, low-maintenance system

For example, a young professional with stable income and fewer responsibilities may benefit greatly from this rule.

Who Should Consider Other Budgeting Methods?

If you have complex finances—such as a family, multiple debts, or fluctuating expenses—you may need a more flexible approach.

In that case, consider:

- Budgeting apps that track spending automatically

- Flexible budgeting systems

- Zero-based budgeting methods for precise control

Final Thoughts

The 50/30/20 rule is a powerful starting point for anyone looking to take control of their finances without feeling overwhelmed. While it may not be perfect for every situation, it provides a clear structure that promotes balance between living for today and saving for tomorrow.

Remember: There’s no one-size-fits-all budget. The best budgeting method is the one you can stick with consistently and adapt to your lifestyle.